BharatPe Turns The Super App Switch On

It’s been nearly 10 months since we first peeked into BharatPe’s plans for the consumer fintech space. Those were the initial days of the fintech convergence, where every app was looking to become a super app.

In fact, with the troubles for Paytm in 2024, this industry-wide move towards super app or fintech platform strategy almost seems prescient. The platform play is evident when we see the product launches from the houses of PhonePe, CRED, Groww, Google Play, Jio Financial Services (JFS) and now, even Flipkart.

Many of these are built around UPI, with the exception of Groww, but BharatPe was already different from many of these apps. It’s always been a merchant-first platform, and so when the leadership told us last November about how it planned to take on the consumer super apps, our scepticism was not unwarranted.

The competition was not exactly light weight here. And that was last November; since then they have bulked up. So when BharatPe finally showed its super app cards this week, we couldn’t help but wonder: is it too little, too late?

Let’s look to answer that, after this short detour into the top stories from our newsroom this week:

- CRED’s Super App Revenue Stack: Speaking of super apps in India, the Kunal Shah-led fintech giant has added more pieces to its platform play this year. We dive into how CRED has changed its outlook towards monetisation in the past two years

- A Game Of Returns: Big exits with large returns have always been a sore topic for Indian VCs. But this situation may be changing with more and more exit events being seen in 2024 thanks to IPOs and secondary deals. Here’s a look at the state of VC exits in India

- The Empire That Was: The odds are stacked against BYJU’s founders Byju Raveendran and Divya Gokulnath, and it all seems to be going awfully wrong for the edtech giant that once was a poster child for Indian tech. We look back at how the BYJU’S empire failed

A Page Out Of Paytm

In some ways, BharatPe has built its super app platform using Paytm as an ideal. In this comparison, we are talking about Paytm from around September last year, when the company was on the verge of turning profitable.

Leveraging Paytm Payments Bank, the company was firing on all cylinders — particularly lending — to get out of the red. But that was not meant to be. In the past year, not only has Paytm lost its key competitive advantage of the payments bank but also some of the trust that had been created among other lending partners.

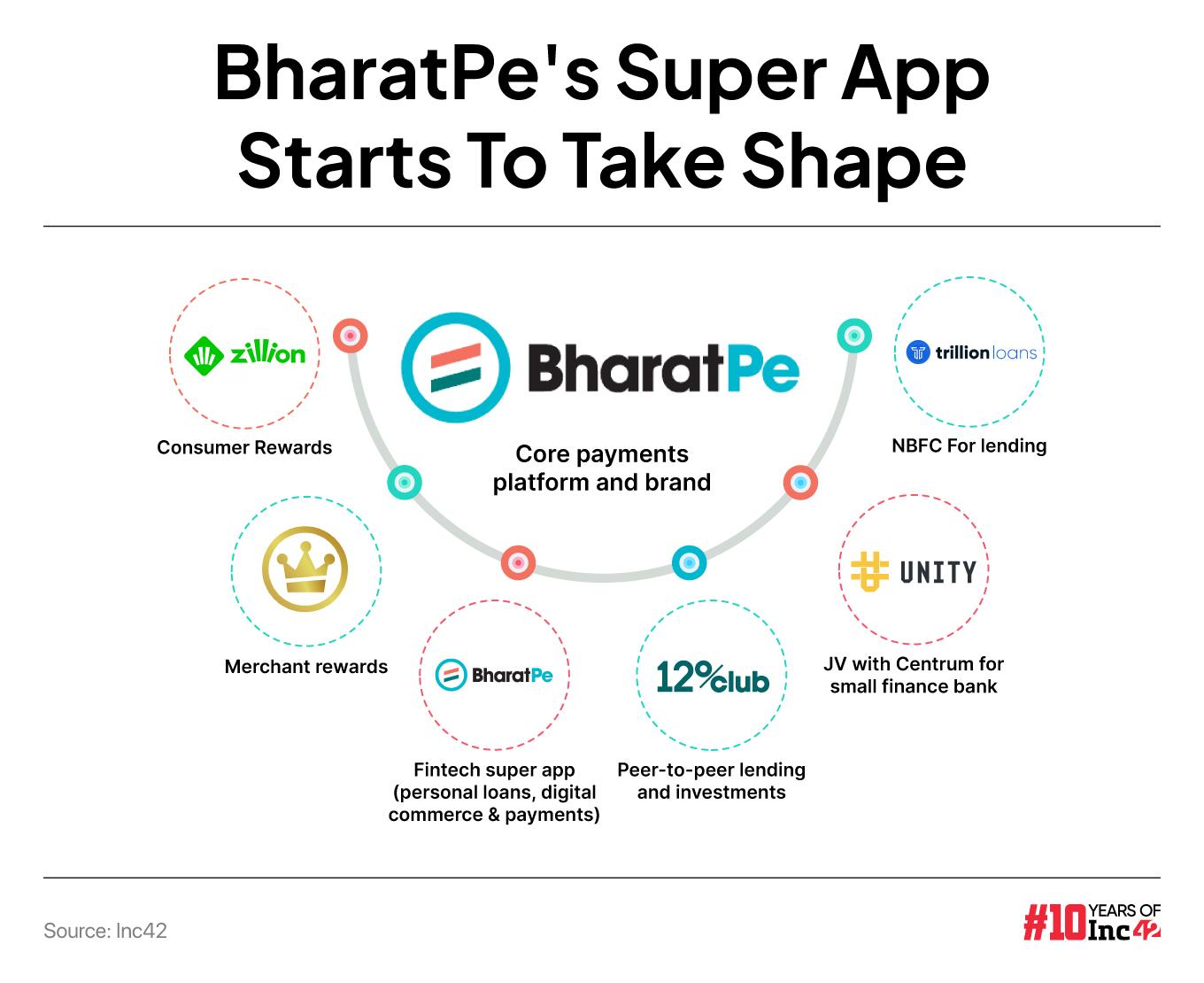

Now BharatPe is looking to fill that void of an app that has a bank as its competitive moat. The Unity Small Finance Bank, in which BharatPe has 49% ownership, is one of the key cogs of the startup’s plans to launch a super app.

Having rebranded its postpe BNPL app to BharatPe, the company is making it a one-stop shop for all services. UPI accounts on BharatPe will have the @bpunity handle, and these can be used for payments for bills, utilities, merchants and other users. Pretty much like any other UPI app. In fact, the company says as much on the Play Store: “BharatPe UPI – Another UPI but the only UPI Made for Bharat”.

It’s clear that BharatPe is promoting itself as an UPI app for the masses. And as such, it will have to build a significant user base to capitalise on the Unity Small Finance Bank (SFB) support. But a super app cannot be about payments alone — it requires a universe of interlinked products. Does BharatPe have that?

Caught In The UPI Paradox

At this point in time, we can safely say that UPI usage is heavily influenced by discounts and cashbacks offered to users. The user experience is more or less the same, so users are more prone to using the apps that are offering the highest discount on every transaction through cashbacks or other means.

BharatPe says its USP is that it will have one of the most secure payments platforms, thanks to the Unity SFB which is an RBI-regulated entity. However, one can safely assume that BharatPe cannot just rely on the bank as a way to attract and acquire users.

For the average end user, the security of a UPI transaction is not as big an attraction as getting a few rupees back for every transaction.

We have written about the UPI paradox in the past, which is a paradox that all super apps have to deal with. By itself, the payments network is not a profitable revenue stream, but without UPI, most super apps do not have a cheap entryway for users to enter their walled garden.

CRED faced this conundrum when it made a belated entry into UPI payments. While the company’s market share in UPI has grown, we cannot say for certain that it has been a profitable route since we don’t know the company’s FY24 numbers.

The goal of course is to keep users coming back to the app and intelligently sell other services. It’s not possible to build a super app with just UPI.

What does BharatPe have in that regard?

Pieces Of The BharatPe Super App

We signed up for the new BharatPe experience and the app itself has a new look and feel that does add to the experience.

Besides UPI payments, bill payments and credit card repayments — bringing in revenue through commissions and fees — BharatPe has added an ecommerce section where it’s currently selling vouchers for Amazon, HealthifyMe, ixigo, Nykaa, Zomato as well as several modern retail and D2C brands.

This is arguably the foundation for a larger marketplace that BharatPe may launch in the future. The startup certainly has ecommerce ambitions because the revamped super app also has an ONDC-powered food delivery service.

With the new app, BharatPe is also offering unsecured personal loans up to INR 15 Lakh via NBFC partners such as L&T Finance, CASHe, and True Credit.

Besides this, BharatPe has the 12% Club, which is an investment platform for peer-to-peer lending and investments, as well as Zillion, a rewards and loyalty program which involves virtual coins a la CRED Coins.

What’s Missing?

What’s lacking is a major payment aggregator licence for which BharatPe has received an in-principle approval, but it cannot yet operate as a PA and therefore it cannot yet become a middle-man between customers and merchants for online payments.

The Delhi NCR-based unicorn also lacks a payments gateway product, which is increasingly being seen as a way for fintech companies to become a part of in-app payments.

Just this week, PhonePe launched PG Bolt, its in-house solution for merchants to integrate a PhonePe payments gateway into their apps and stores.

BharatPe’s go-to-market strategy of merchants first and then consumers means that it will now have to match some of the upfront investments by the likes of PhonePe, CRED, Google Pay and others to acquire users.

In the eyes of many, acquiring consumers is tougher as consumers easily jump from one UPI app to another.

Acquiring merchants is also costly, but it involves lock-ins and subscriptions that can pay off over the period of usage. Pretty much every major consumer payments app has made inroads towards the merchant side with a view to building a double-sided network of consumers and merchants that can be leveraged to cross-sell other services.

Super Apps Are Expensive

BharatPe is joining this wave from the other side, with Nalin Negi as the full-time CEO now, who was appointed at the beginning of this financial year.

In April this year, the company claimed to have witnessed 182% increase in revenue from operations in FY23 and achieved its first EBITDA positive month in October 2023. In November last year, it also claimed that its “annualised revenue” crossed INR 1,500 Cr for FY24, a 31% increase from FY23. However, these figures were not audited at the time and haven’t been filed by the company officially.

So we don’t know whether BharatPe broke its loss-making streak in FY24. We suspect that the company will continue to be in losses given how much work was needed at the end of FY23. While the revenue breached the INR 1,000 Cr mark, BharatPe’s net loss was almost the same as the income at INR 926.9 Cr.

BharatPe had INR 508 Cr as cash and cash equivalent at the end of the fiscal year, which the company will look to leverage as it expands into new areas. The startup will need to spend on marketing, invest in brand-building exercises. acquire and retain users through discounts and cashbacks, and also bring partners on board for ecommerce, lending and other consumer verticals.

At the same time, it cannot afford to step off the accelerator for merchants either. Its most recent launch was the BharatPe One, an all-in-one PoS device for cards and UPI transactions. It plans to push the presence of this device to 450 cities by the end of the year.

What we know is that the super app strategy can have a real payoff for startups if they manage to get their products right and trigger cross-selling at the right junctures. PhonePe, for instance, claims that its revenue in FY24 grew to INR 5,064 Cr, largely due to the diversification of revenue streams and cross-selling.

So the upside is clearly there. We can see a similar boost for CRED and the likes when their individual products mature and add to the bottom line.

Now, let’s come to the question of whether BharatPe is late to the party. The popular argument is that India has plenty of depth for multiple large players in the same sector. The UPI transaction share cap is also a factor. Both are valid arguments, though we don’t yet know whether BharatPe has the right product mix to tap this depth.

Another significant challenge will be fighting off the more mature super apps who have more verticals to offer, more customers to bank on when fighting off the competition and are more firmly embedded as brands in the consumer’s mind. And that’s not even counting the might and reach of Reliance and Jio Financial Services, which is also going the super app way.

Finally, how much of a factor will Ashneer Grover continue to be for BharatPe? The former MD and cofounder of the company is still in the midst of a few legal battles with the company and there is the matter of the Economic Offences Wing probe. Will these ghosts of the past continue to haunt the new BharatPe?

BharatPe has taken its sweet time getting here. Is it too late to the super app party?

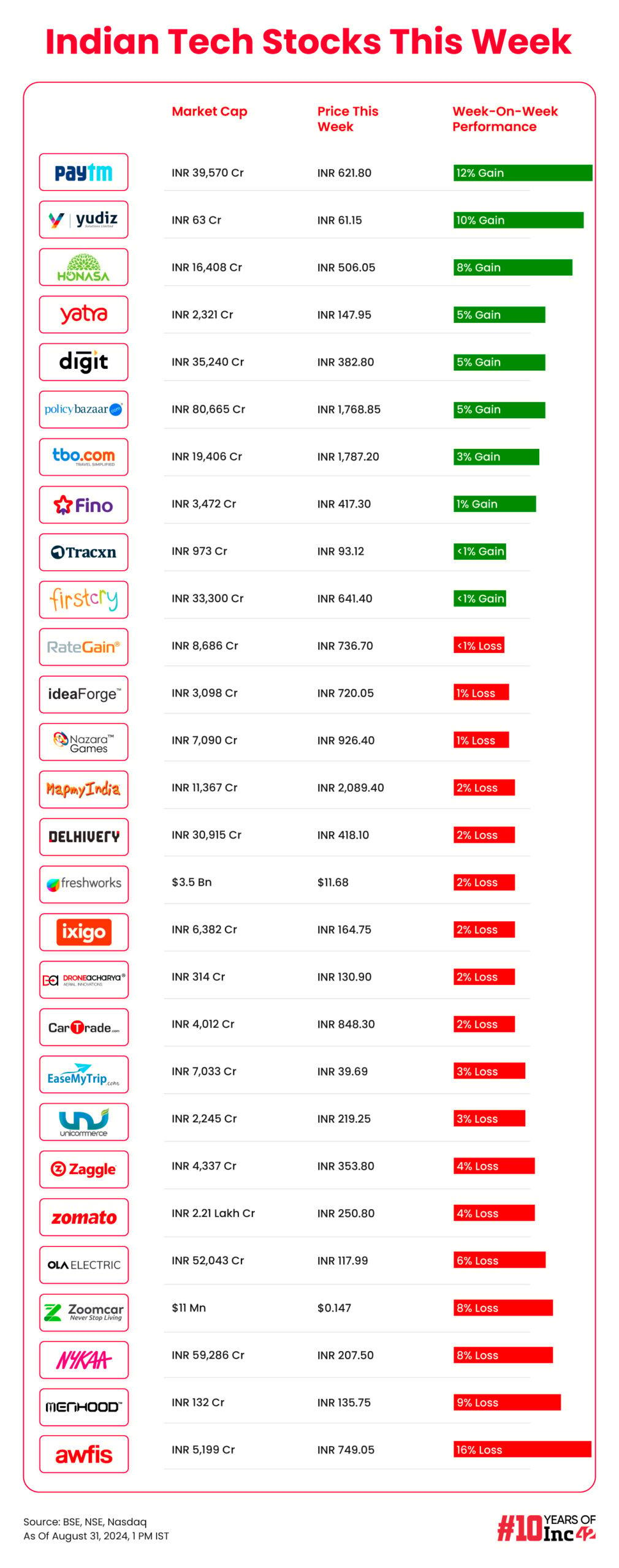

Sunday Roundup: Startup Funding, Tech Stocks & More

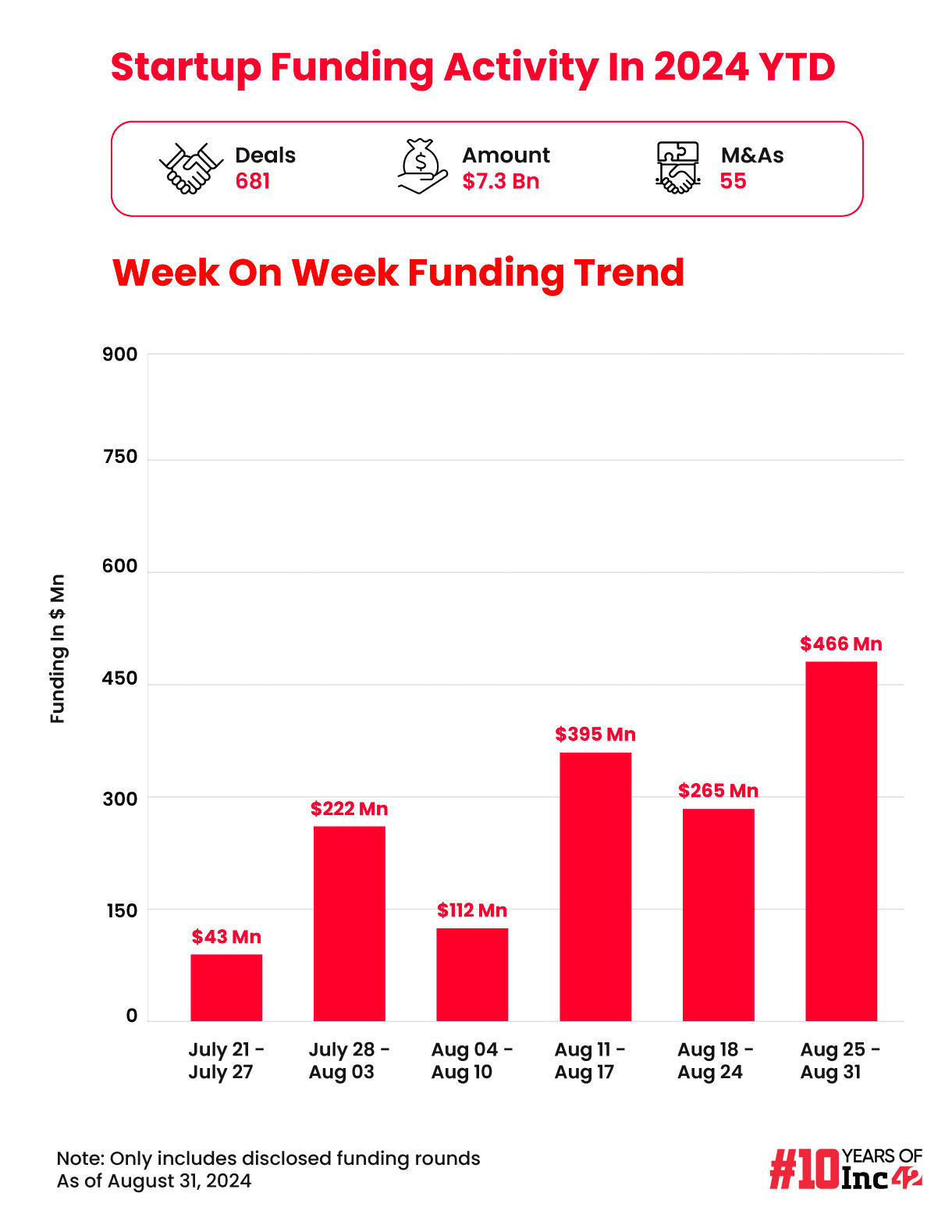

- Zepto’s $340 Mn round dominated the total funding tally for Indian startups this week, with $466 Mn raised across 22 deals

- Cash-strapped Dunzo has fired 150 employees in a fresh round of layoffs, leaving just 50 employees in the company for the supply chain and marketplace verticals

- With yet another acquisition, Dailyhunt parent VerSe Innovation is looking to boost digital advertising and marketing revenue. Will the plan work?

- Newly-listed Unicommerce saw its net profit zoom 31% YoY to INR 3.51 Cr in Q1 FY25, largely on the back of improved operational efficiency considering the relatively slow YoY revenue growth

- Firstcry pulled back its net loss by nearly a third to INR 75.68 Cr in Q1 FY25, its first quarterly results after the public listing last month

- Reliance Jio made a huge AI play, announcing multiple new products for its telecom subscribers as well as enterprise automation through Jio Brain

The post BharatPe Turns The Super App Switch On appeared first on Inc42 Media.

No comments