Digit IPO: Litmus Test For Insurance Tech

Nearly two years ago, Go Digit was set for an IPO. But market conditions, SEBI regulations and more put that plan on hold.

But the insurance tech unicorn is back for another shot at a public listing, and this time around, the IPO is definitely happening. The company has set a price band in the range of INR 258 to INR 272 per equity share for its upcoming INR 1,125 Cr+ initial public offering, which is opening for bids on Wednesday, May 15.

With this, Go Digit is becoming one of the first major IPOs of 2024. And other companies are lining up in 2024 and 2025 to join the insurance tech unicorn. So in many ways, the Digit IPO is one of the most critical ones for the Indian startup ecosystem since 2021. Which way will the coin fall for Go Digit?

We look to answer that, but first, a look at the top stories of the week:

- Big Questions For Swiggy: Like most loss-making startups, Swiggy has to answer plenty of questions ahead of its IPO. Here are the five major ones ahead of the $1 Bn+ IPO

- Unacademy’s Profitability Push: The edtech giant’s medical entrance test prep platform PrepLadder has undergone another round of layoffs amid a shift in Unacademy Group’s sales strategy to streamline costs

- Paytm’s Big Shift: With several key business heads exiting Paytm, a lot rests on how the new leadership works under the direction of founder and CEO Vijay Shekhar Sharma to revive the company

The Question Of Valuation

The first thing we have to turn our attention to is the valuation for Go Digit or the pricing for the IPO. The insurance startup is going for an IPO at a discount of 25% to its last known private market valuation, which is largely a result of how much things have changed in the past two years.

At a price band of INR 258 to INR 272, the company is eyeing a valuation of $3 Bn (approximately INR 24,000 Cr) on the higher band. However, its last private valuation in 2022 was $4 Bn (close ot INR 32,000 Bn).

At the pre-IPO briefing on Friday, Go Digit founder and chairman Kamesh Goyal said the price band will leave plenty of value on the table for investors, and is in line with what investment bankers have advised the company.

While the class of 2021 might have tried ambitiously to list at super-high valuations — Paytm being a prime example— the past two years have shown the reality of the market for companies such as Digit. More and more Indian startups, particularly those at the later stages, are realising that the valuation terms of the past are history. Now, companies are more than happy to raise money at lower valuations as long as survival is possible, no matter if they are private or going for a public listing.

In fact, for a unicorn, Digit is going for a relatively small listing. In terms of fresh funding, the company is looking to raise INR 1,125 Cr, while the offer for sale from existing shareholders has also been halved to 54 Mn shares from 109 Mn shares as stated in Digit’s previous IPO filings.

Digit’s valuation expectations are still relatively high compared to other insurance players in the market. In fact it’s quite a bit higher. The higher price brand would result in a 680X multiple for Digit on revenue basis, whereas the insurance industry leaders are close to 43X.

Investors we have spoken to believe that given the low penetration of insurance in India, high valuations are a norm. Plus many investors believe that insurance tech is only going to grow larger with new models of underwriting, the increase in data and high growth ceiling for business-related insurance products.

“The Indian non-life insurance market will grow at 13-15 per cent in the medium term. The industry’s growth will be primarily driven by the health and motor insurance segments, supported by increasing disposable income levels and a rise across other segments,” ratings agency CareEdge said in an April 2024 report about the Indian insurance space.

So let’s look at the two major categories it is targeting that will determine the course of the general or non-life insurance space, and how Digit is placed in this regard.

The Digit Network: Motor Vs Health Insurance

There is no denying that Digit is seeking the valuation multiples of a typical tech startup, while being in the insurance business which is tightly governed by regulations. In fact, in the early days of the startup, Digit relied heavily on the digital onboarding of customers, and in the past few years, this reliance has gradually reduced.

Online direct selling is still relatively small for Digit and other players, as compared to human agents selling insurance plans and onboarding users after KYC. Even a digital insurance platform cannot be completely online, and has to work as the traditional players do because of the high bar for regulatory compliance.

This is why today, Digit has a network of 61K+ distribution partners and nearly 59K sales agents on the ground. According to the company’s revised DRHP, Digit expects the majority of its customers to be acquired through its agent and broker network, which is to say that the company has to increasingly look at the model which has been popularised by LIC, and followed by other players, including insurance tech companies like InsuranceDekho.

Much of Digit’s network is geared towards selling motor insurance. This comprises 61% of Digit’s business, while health insurance is a distant second at 14% of the gross premium received by the company in FY24.

Because motor insurance is mandated by law for all vehicles, this is a highly competitive segment and there’s no real moat for companies except low premiums and discounts on insurance plans. Health insurance is the true underpenetrated product.

Digit’s share of the overall health insurance market is just around 3%. This is the big opportunity that Goyal will be targetting after raising capital from the public markets.

Analysts believe that Digit will have to up its game across multiple insurance products to continue the premium growth that justifies its valuation multiples which are quite rich compared to listed companies.

Growing Profits Are Key

The only factor that can help Go Digit swim against this tide is profitability, and here, there may be some merit to the company asking for high multiples from the market.

According to General Insurance Council data, Digit had a gross written premium (GWP) of INR 7,941.1 Cr in FY24, which is nearly 30% higher than the INR 6,160.08 Cr it recorded in FY23. However, Go Digit’s RHP only has data up to December 2023, when GWP was at INR 6,679 Cr. When comparing the GIC data to Digit’s FY23 numbers, we can see an increase of just under 10% in GWP.

In comparison, the nearest insurance tech competition is Acko, which had a GWP of INR 1,870 Cr in FY24 and INR 1,509 Cr in FY23. This is an increase of just under 24%, which is more than 2X of what Digit saw, highlighting that a relatively low revenue base is not a disadvantage for Digit’s competition.

This is yet another indicator of the low insurance penetration in India.

For the first nine months of FY24, i.e as of December 2023, Digit sharply brought down its operating loss to INR 10 Cr, while profit after tax (PAT) stood at INR 129 Cr.

Chairman Goyal said the loss is small at operating level and not meaningful to impact the company’s services. “Most of our business is retail, so expenses will be high. If you look at our AUM in the last 6 years, it has been more than 15% of some of the top 5 companies. When you are growing fast, it leads to losses because your commission expenditure has to be expensed on day 1 while revenue is earned over a period of 365 days.”

As for the category split and the heavy reliance on auto or motor insurance, Goyal acknowledged that health insurance has to become the key focus for Digit going ahead. “Our health (insurance) business has doubled over the years. The loss ratio was good at a time when everyone was losing. We doubled our premium in one year. In three years, it will be the fastest-growing category for us,” he said.

Three years is a long time and competition in the insurance space is only expected to grow. So, while Goyal may be optimistic, there’s a lot that Digit has to prove before it can claim for certain that the IPO valuation was on the mark.

The New IPO Wave

However, Digit’s IPO is important for other reasons. Before we wrap up, let’s take a moment to see why the Digit IPO is a big deal for Indian startups and tech companies.

The Digit IPO is not just vital for the company but also a test of the Indian startup ecosystem, and something of a report card on the past three years.

After PB Fintech, Nykaa and Paytm got their listings in November 2021, Go Digit is the next major new-age tech company going for an IPO. It’s been three years, and in that gap a lot has changed. Unicorns have largely delayed their IPOs, including the likes of OYO, boAT, Pine Labs and others, besides Digit.

So many entrepreneurs and public markets investors would be watching the fate of Digit now, because it will give them a hint about how other IPOs might be received. Besides the insurance unicorn, other key public listings expected in 2024 include FirstCry, PayMate, Awfis, Mobikwik, Ola Electric and OYO, and Swiggy is expected to join this group by later this year. There’s a bit of pressure on the startups of an older vintage to get those returns for investors.

As per an Inc42 ‘s 2024 u, 95% of investors believe that IPOs would be the most popular exit route for startups in 2024, given that most M&As are going through only because of their distressed nature. Essentially, IPOs are becoming a reality for investors, even though the valuation maths is still very critical.

For many of those who backed Digit, as early as 2016 when the company was founded, this is a vindication. These investors are all but certain to make a lot of money from the Digit IPO, given how these things usually work.

But as far as the public markets are concerned, the key to future value creation will be profits and profits alone. Will Digit’s rich valuation be able to sustain itself as the company adds to its revenue base?

That is a critical question that is likely to be answered later this month. And another big question is: will the public market response to Digit determine the fate of other massive Indian startup IPOs in 2024?

Sunday Roundup: Tech Stocks, Startup Funding & More

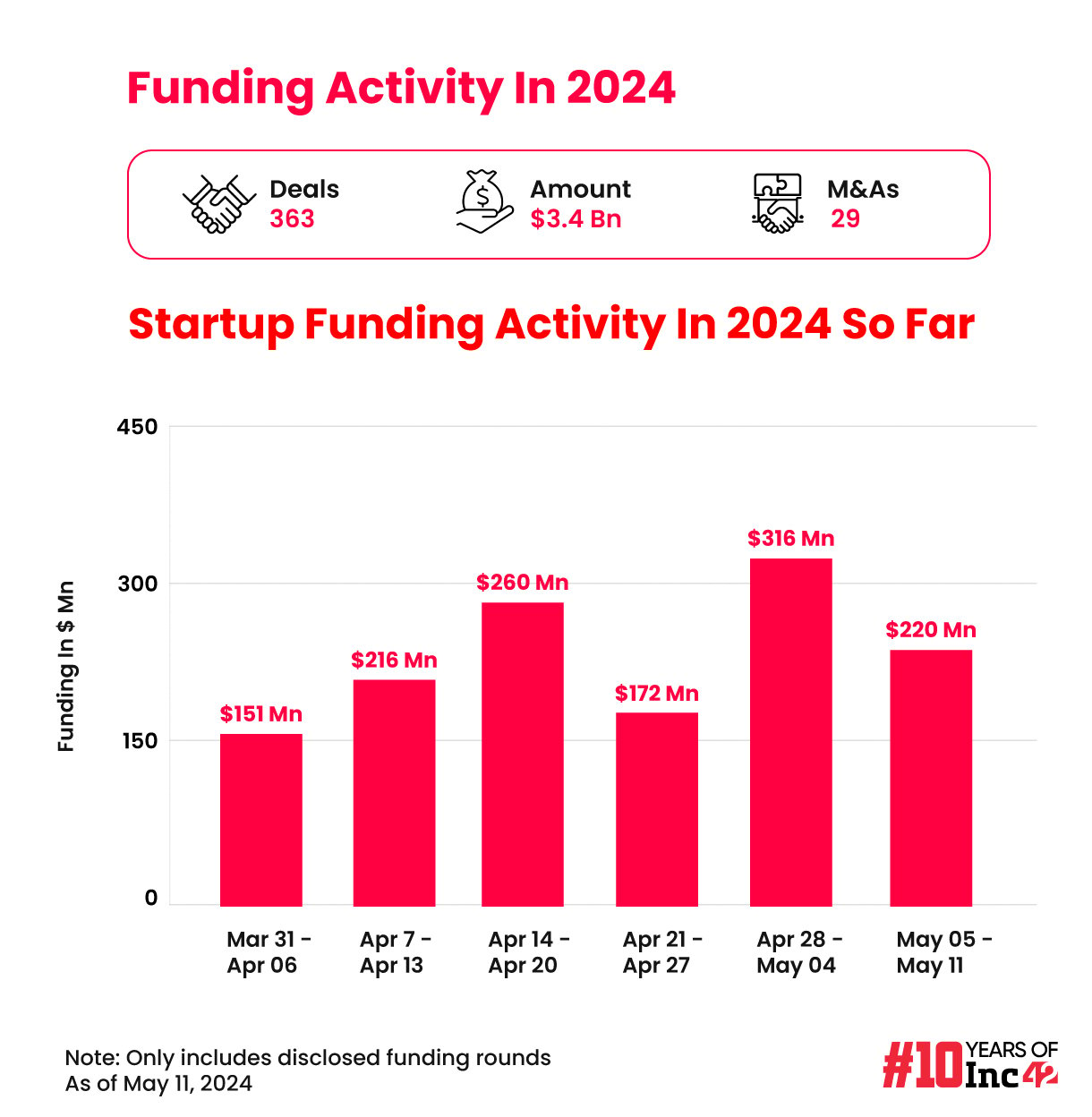

Weekly Funding Drops: Startup funding was a low-key affair this past week as compared to the previous one, with just over $220 Mn raised across 21 deals, a 30% decline week-on-week

Groww ‘Returns’ To India: Fintech unicorn Groww has completed its reverse flip, shifting its domicile to India from the US, merging the holding company Groww Inc with its Indian entity Billionbrains Garage Ventures Private Limited

Bhavish Aggarwal’s Feud: Amid a tussle with Microsoft-owned LinkedIn over a post on the use of genders in AI, Ola chief Bhavish Aggarwal said that Ola would stop using Microsoft’s Azure and migrate to a native cloud platform, but is this easier said than done?

TBO Sees Big Bids: B2B travel portal Travel Boutique Online received an overwhelming response for its IPO, with 86.7X subscriptions as of the final day for bidding

The post Digit IPO: Litmus Test For Insurance Tech appeared first on Inc42 Media.

No comments