Paytm’s Lost Postpaid Magic

Just when Paytm seemed to be on track to hit profitability, there’s another speed bump. And this time around, Paytm doesn’t just have to slow down but also swerve to avoid a crash.

This week’s withdrawal of the company’s low-ticket Postpaid feature or buy-now-pay-later (BNPL) service has created a difficult situation, as this was one of the key success factors for Paytm’s profitability in the past few quarters.

And while Paytm has denied that this is the end of BNPL on the app, it’s looking increasingly like that given that the new focus is higher ticket loan sizes.

The BNPL loan book had become a critical monthly recurring revenue for Paytm and the changes could derail Paytm’s run towards profits. But before we look at that, let’s take a detour into the top stories of the week from our newsroom:

- ZestMoney’s Last Days: ZestMoney is shutting down after a torrid time this year. But what happened at the fintech startup that was flying high at one time? Here’s a look at the last few days of ZestMoney.

- Year Of Shutdowns: More than 15 startups had to shut shop this year after being pushed to the brink by tough market conditions — Pillow and FrontRow were some of the big names that bit the dust in 2023

- Layoffs At Simplilearn: Inc42’s exclusive report on how Blackstone-owned edtech giant Simplilearn has laid off 200 employees citing performance reason, which employees allege is not the full picture

Paytm Postpaid’s New Avatar

First, let’s understand the sequence of events leading up to the changes at Paytm. In late November, many users reported on Twitter about being frozen out of Paytm Postpaid.

Then reports emerged this week about Paytm halting Postpaid operations, which the company denied after a swift press conference. Finally, in a call with investors and shareholders, Paytm said it is not halting Postpaid, but recalibrating the portfolio origination of less than INR 50,000.

It claimed to have taken this call on the back of recent macro development and regulatory guidance, in line with its focus on driving a healthy portfolio. “While we’ll continue to do postpaid, and it may not be the same growth level that we were doing earlier, it will be significantly lower than what we were doing earlier, but it will be a product that will continue,” the fintech major told investors.

Given the recent RBI directives to banks and NBFCs to increase the risk weights — the amount of cash banks need to reserve to service risky loans — which has forced the banks and NBFCs to reassess their portfolio. As a result, agreements with the likes of Paytm which offer small ticket loans are being reassessed.

One Delhi NCR-based fintech founder says even banks and NBFCs need to show improved profitability and these small loans do not contribute to their bottom line significantly.

What Postpaid Means To Paytm

Losing the key low ticket size segment of Postpaid is a blow to the company’s financials. While it has admitted that future growth will be slow, the company would also be wary of value erosion due to any slowdown in its lending business.

Paytm has posted staggering growth in the lending vertical in the last quarter i.e. Q2 FY24, where disbursals increased to 1.32 Cr loans (44% higher YoY) and the total loan amount to INR 16,211 Cr (122% higher YoY).

But how much of that is from Postpaid and what can we expect come next quarter?

The Postpaid vertical has historically contributed the biggest to its lending business in terms of value. In Q2, Paytm disbursed Postpaid loans worth INR 9,010 Cr, which is 12% higher than what the company did in Q1. Interestingly, loans under INR 50,000 made up to 75% of the total disbursements, and this entire chunk is more or less out of the picture.

Even if we assume some overall growth for Postpaid in Q3 FY24 (December 2023), Paytm is looking at significantly lower revenue on the lending side.

The nature of Postpaid meant that a lot of Paytm’s young users without credit cards were using the BNPL credit line like a credit card. Postpaid also had wide acceptability in the offline merchant space, making it more attractive than the likes of LazyPay and others which offered a similar feature.

Paytm’s Value Tied To Lending

For Paytm, the decision to defocus from the low ticket size means that it will likely lose out on the traction it sees from users due to Postpaid usage. It’s a double blow along with the revenue, and one which has decimated Paytm’s stock.

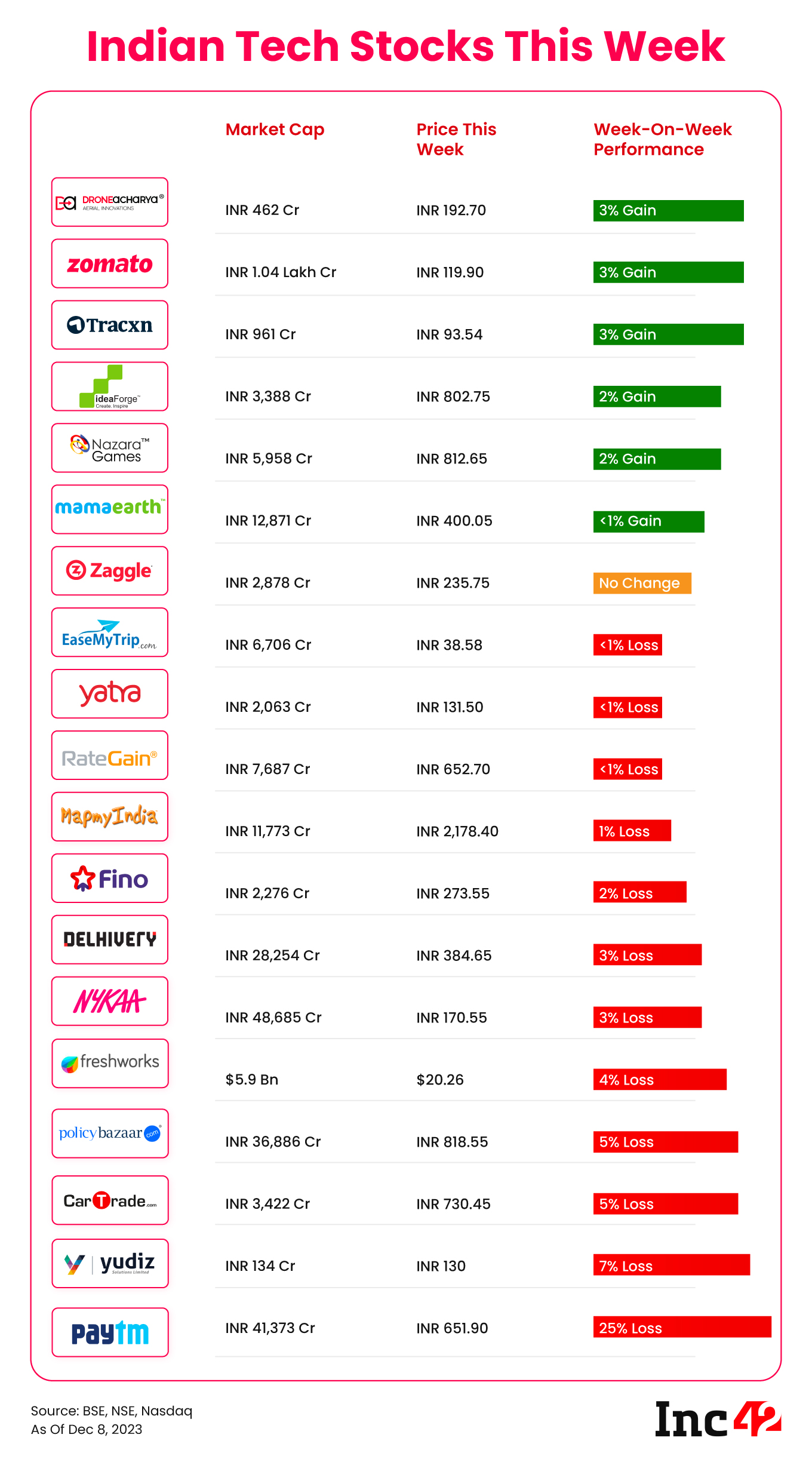

After a rally throughout most of the last few months, Paytm’s market cap tumbled from INR 55,256 Cr to INR 41,373 Cr in a week, a fall of 25%.

Brokerage Motilal Oswal believes Paytm’s loan disbursement run rate is expected to decrease from INR 6,000 Cr per month to about INR 4,500 Cr. “Paytm adds an average 3.5 Lakh to 4 Lakh customers every quarter, which is now expected to come down by 50%,” the firm claimed.

Similarly JM Financial noted that Paytm’s FY24 estimated loss before tax is likely to increase by 11% as a result of the changes.

BNPL’s Time Running Out

But of course, BNPL was never a reliable ship. The segment has had its share of worries for a long time. Plus, this particular Paytm episode highlights the weakness of relying on a base of low-value loans.

Analysts expect several other companies to also focus more sharply on higher loan tickets where a higher standard of risk assessment and diligence is needed, rather than the blitzscaling of BNPL startups and the associated irresponsible lending.

“BNPL was always a sticky wicket and it’s no surprise when you see that with each RBI intervention, the segment sees great pain. And even the valuation bubble is now burst, so the time is for responsible lending and not spraying capital around,” said one Delhi NCR-based fintech founder.

BNPL startups such as Simpl and Slice which had models similar to Postpaid’s credit lines have pivoted to other models since then, and even Lazypay introduced personal loans to hedge against any slowdown in BNPL.

Speaking to Inc42, Kissht/RING founder Ranvir Singh added that lending by itself is too big and too ingrained into the economy to slow down. What we might see is better governance standards in lending operations. Kissht claims to have an average ticket size of INR 1.1 Lakh.

“Though risk weights for unsecured loans have increased, there is an elevated interest from lenders and co-lending partners to disburse loans greater than INR 50,000. This will further usher an era of more responsible lending where credit worthy customers will continue to be served adequately,” Singh said.

Can Paytm Refocus?

For Paytm, the answer lies in adding more partners for its personal and merchant loans, where it will be looking to make up most of the lost Postpaid revenue. These areas are typically more lucrative for revenue and long-term profits, but building a large loan book requires a lot of legwork.

In the initial days, Paytm is likely to have to spend heavily on customer acquisition and even then it will need to keep a high bar for disbursing loans. Shifting focus to larger ticket loans is not without challenges, given that besides higher risk weights, there is the FLDG component, where partner financial institutions are likely to ask digital lenders to put up collateral.

Lending might continue growing as a whole, but Paytm will have to fight harder for its share of the pie.

2023 In Review: Recapping The Highs And Lows

As 2023 draws to a close, it’s time to reminisce about everything — from the key deals to breakthroughs from trends to controversies in the Indian tech & startup ecosystem. Like every year, Inc42 launched 2023 In Review in late November and throughout the past few weeks, we have captured the year through snapshots and analyses.

This week, we looked back at the startups that turned profitable in FY23 and set off on a new trajectory. Plus, our roundup of the sport stars and athletes that turned investors, as well as those who continued to back new-age ventures. And while 2023 was not a massive year for IPOs, some startups managed to buck the trend and go public despite tough market conditions.

Bookmark this page to see what we have in store!

Sunday Roundup: Tech Stocks, Startup Funding & More

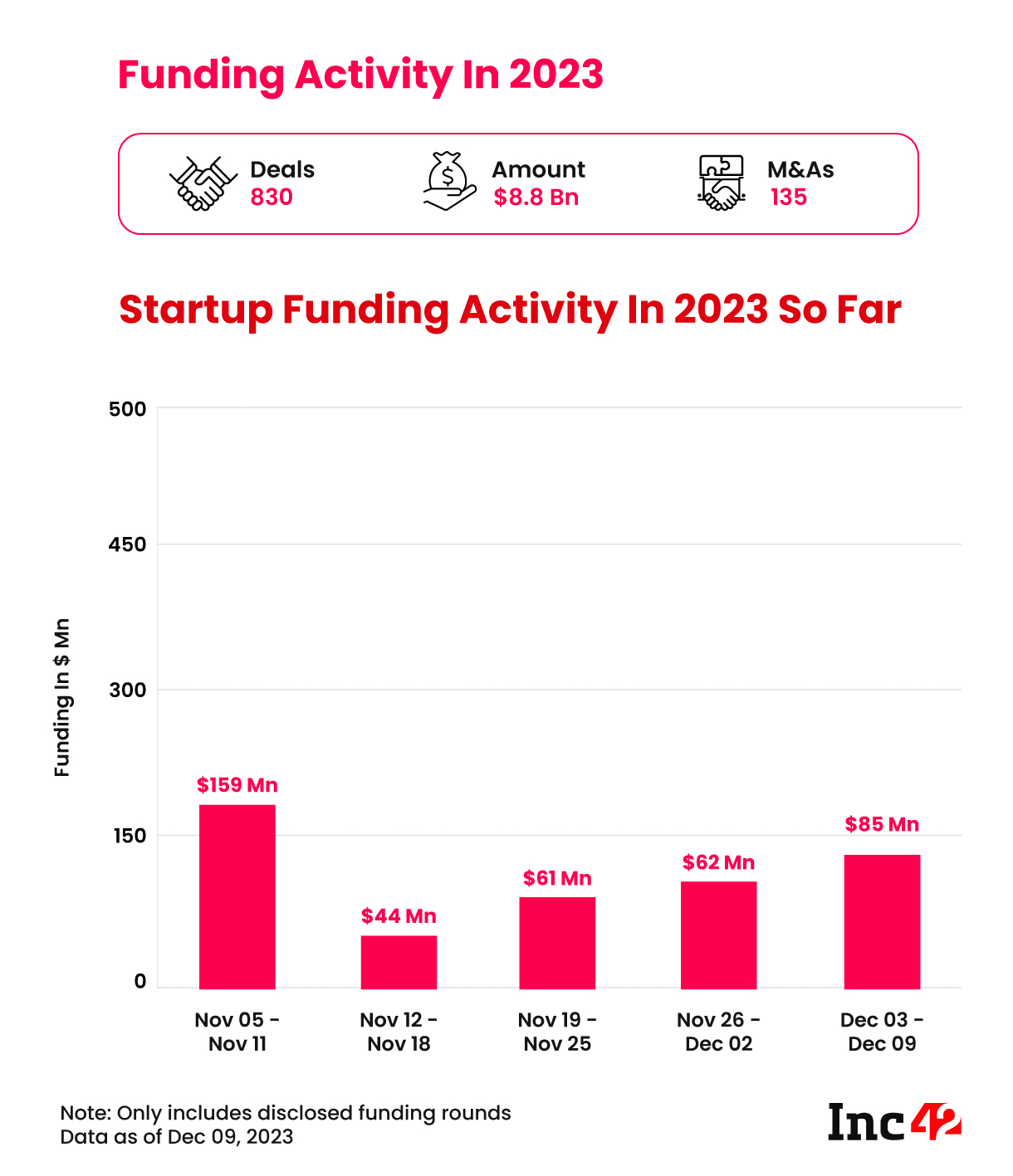

- Slow Year For Funding: With the year about to close, Indian startup funding is likely to just breach the $9 Bn mark. Between December 4 and 9, startups raked in $85 Mn across 18 deals

- OpenAI’s India Plans: Sam Altman-led OpenAI is reportedly partnering with former Twitter India head Rishi Jaitly to help facilitate talks with the Indian government about AI policy

- SoftBank Sells Zomato: SoftBank offloaded 9.35 Cr shares of foodtech giant Zomato this week in an INR 1,127 Cr block deal, most likely completely exiting its position

- Another Boost For UPI: The RBI has proposed increasing the INR 1 Lakh limit for UPI payments to hospitals and educational institutions to INR 5 Lakh per transaction among other changes

That’s all for this week folks. We’ll be back next week with another roundup as we close the curtains on 2023.

Don’t forget to stay tuned to our social media channels during this time of the year. Join Inc42 on Instagram, X/Twitter and LinkedIn for the latest news as it happens.

The post Paytm’s Lost Postpaid Magic appeared first on Inc42 Media.

No comments