Five Years In The Making: CRED’s Year Of Vindication

CRED doesn’t do labels — ask the company to name its key leaders, and there’s no straight answer. The refrain time and again is about functional teams and high ownership across the ranks.

But I wasn’t at the company’s new second office in Bengaluru to discuss official designations. Instead, we wanted to dive into the year that went by with the leadership. And I couldn’t help but notice an airier, more open version of the company which is otherwise quite guarded.

After all, 2023 is a big year for CRED — it’s about the coming-of-age for the company’s products and embracing the platform life and proving that financially too, it is on the right track. With new products that could add significant revenue momentum, CRED is answering many who had questioned its business model for years. This year was also about showing that building patiently and slowly has its rewards.

With its new office, the Kunal Shah-led startup has now bookended an entire block on Indiranagar’s 100-foot road, creating what can only be described as the CRED bubble.

The CRED bubble is, of course, not a bad thing. It’s largely indicative of Shah’s outsized influence on the Indian tech ecosystem. Naturally, most people associate CRED with its founder — the only designation that cannot be hidden.

But still we were curious to know who leads other key parts of the business. No clear answer. What’s your role, we asked Miten Sampat. He played out pretty much the same tune, even though everyone knows he’s been a key figure in the CRED infrastructure for the past few years.

Sampat, who was the Times Internet chief strategy officer for five years before joining CRED in 2020, works across the public relations and government relations team, the finance function, legal team, strategy, and investor relations.

He is someone who has the ringside view of the journey, how the long-term platform vision fuels CRED’s products engine and works close-quarters with Shah and other key leaders in the company (unnamed even though they are).

Having completed five years in 2023, CRED is finally opening up, even though it’s awkward about it.

As part of Inc42’s wrap-up of 2023, we dove deep into the year gone by for CRED and unearthed some insights from how the startup builds its products, its relatively slow-burn approach and the questions about profitability.

‘CRED’s Broad Canvas’

For CRED, the benchmark is not Paytm or PhonePe or any other fintech app; it’s Apple and Mercedes — no surprises there (more on this later). It’s the one thing that perhaps sets the startup apart from the horde of competitors in the rapidly growing fintech space.

Every company is gearing up to become an all-in-one fintech app, but CRED claims to have taken a deliberate approach, without compromising on the product ethos — deeply thought-out features, high-quality design assets and UX, and products that fit into CRED’s customer persona model, which make sense for the platform.

“Kunal had a very crisp vision of what the opportunity is, which is that the trustworthy and credit-worthy user base in India deserves better, and can be served in a unique way. That was the broad canvas and that canvas is still the same today,” says Sampat, adding that the primary challenge for CRED from a product vision point of view is choosing what to do next.

Choosing what to do next is not something most startups have the luxury of. In CRED’s case, that’s largely due to the capital raised by the company that allows it to take its time, but it also goes deeper than that. Shah’s reputation as a founder who has seen a big exit also brings a lot of time to grow.

The company has raised over $1 Bn over 10 rounds in five years, so it’s not lacking for capital. But it’s also about knowing what pieces of the puzzle will actually fit next to each other. Sampat says often capital makes you want to do everything and hoping that one of them will work.

“You really cannot do step seven, unless you do step one through six. And then you may imagine I want to do step 27 also, but you don’t get the right to do that until you sort of actively build the layers and things adjacent to it,“ Sampat says.

‘Is This A Delta-4 Experience?’

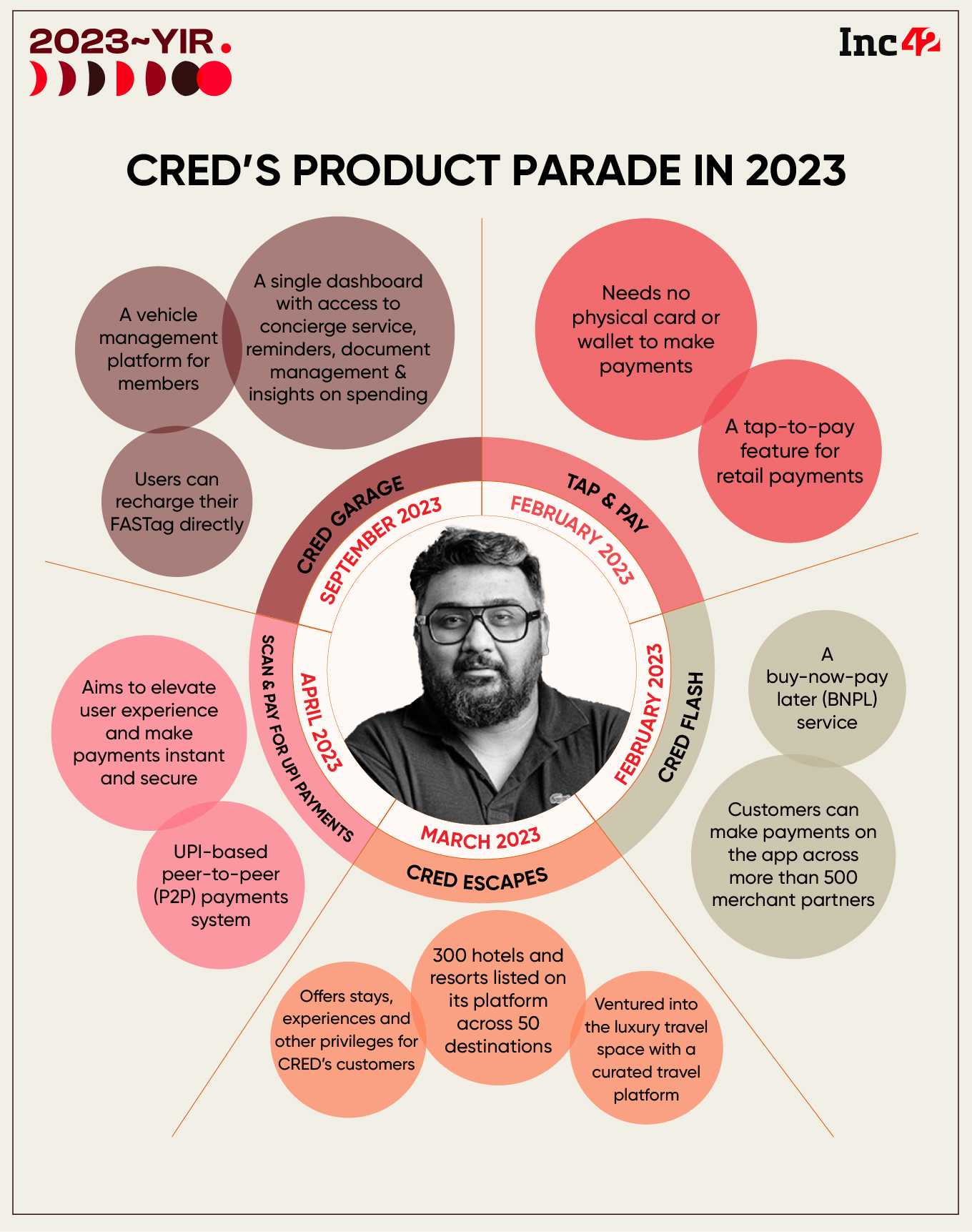

So when did CRED choose to go into something like vehicle management with CRED Garage, which came out of the blue, but fits like a glove within the platform. After the launch, it seems like a very obviously CRED product, but how did the company arrive at that point?

According to Sampat it goes back to the underlying thesis of building for the ecosystem of people who are high-trust, which is based on an objective metric called a credit score. In some ways, this cohort represents the cream of the overall Indian fintech TAM. Essentially, the very premium layer comprising the 100 Mn Indians who own a credit card

“So when we look at the problem statements that they have in their life where we can potentially make a difference. That’s the starting point of how we think about all products, not just Garage. There are some products which we aspire to make, but until we have a unique insight that fits this persona, we’re not gonna go build it.”

The origin point for Garage was more than a year before the launch, when the CRED team was ideating on how to develop a product linked to FasTAG electronic toll payments. By itself, the product would have been just another FasTAG service like Paytm or PhonePe, but the idea was to flesh it out more fully.

Another decisive question that CRED asks itself in the process of product development: ‘can we create a Delta 4 experience’, based on the theory put forward by Shah. Put simply, Shah claims, “Once the user experiences a significantly better way of using a product, there is no way he or she is going back to the old way of doing things.”

Sampat claims a product like Garage doesn’t exist anywhere in the world, and it’s similar to how CRED changed credit card bill payments, which seems like an afterthought today, but it was also a unique product at the time. In the first three weeks, CRED Garage claims to have hit 1 Mn vehicles registered.

As he talks about the building backward from the customer persona, Sampat drops a few hints of what CRED is thinking next: “These are the people who invest in mutual funds, the people who pay taxes, these are the people who own cars, credit cards and passports. I think that at some levels we all feel like this ecosystem is adequately served. But if you dig three levels deep into any problem statement, you realise there’s a lot of opportunity. Things are far from sorted.

Garage is also unique in the sense that CRED did not acquire any companies to build this product, as it has done on the lending side with the acquisitions of CreditVidya in 2022 or Spenny in 2023 or even the likes of Happay in 2021. While these acquisitions are key for CRED’s grander plans in the investment tech and lending space, Garage remains a wholly unique proposition.

What’s not unique is CRED’s UPI play, but even here the company banked on building for the customer persona, which has paid off in a big way.

‘Why’s Yours Black And Why’s Mine White?’

For years, fintech meant payments and payments meant UPI. Startups built user bases through UPI and now realise they need services for revenue, something which UPI does not contribute towards.

In October 2022, when CRED launched UPI payments, we wondered whether it was too late to enter the game. But since the launch, the company has managed to climb up the UPI rankings and is the fourth-most used UPI app in the country today.

The launch of UPI has been critical for CRED to drive engagement among its users and it’s also one of the places where we can see the product philosophy pay off. “It was an important piece in the puzzle as it ties the various verticals together and you can see the impact in terms of the financials and the growth,” says a Bengaluru-based founding partner at an early-stage VC firm that has invested in several fintech startups.

Unlike other players of its ilk, CRED decided to take a gradual approach to UPI, launching nearly half a decade after the likes of PhonePe or Paytm or Google Pay. And it helps that perhaps people want to try new apps for UPI because there is no cost involved with switching apps.

“The paucity of rewards on other apps after five long years meant CRED had the opportunity to offer rewards and syphon off users. Users want rewards and delight, and CRED offers both in spades,” the partner added.

We asked Sampat what led to this quick success for CRED UPI, and his answer is that people use different signals for different transactions.

Someone with multiple credit cards will likely pull out the fanciest one in the right company, and the same could be said about CRED’s UPI play.

Sampat says, “There’s the factor of ‘Why’s yours black and why’s mine white?’ We also focussed on speed, safety and privacy. We have the fastest QR scanner today and we have fraud protection measures, which is basic but no other app has done that.”

The UPI product has been key in converting the user base from low-frequency actions for credit card payments to high-frequency actions like daily small-ticket purchases. And indeed, Garage or CRED Escapes (travel) or the CRED Store are all part of this effort to push up engagement among the most active users.

‘Building Like Apple Or Mercedes’

Products by themselves don’t matter of course. It’s about how they move the revenue needle. For CRED, the FY23 performance is seen as a turning point, but there’s an even more meaningful outcome that the company had been chasing for — higher engagement from its users.

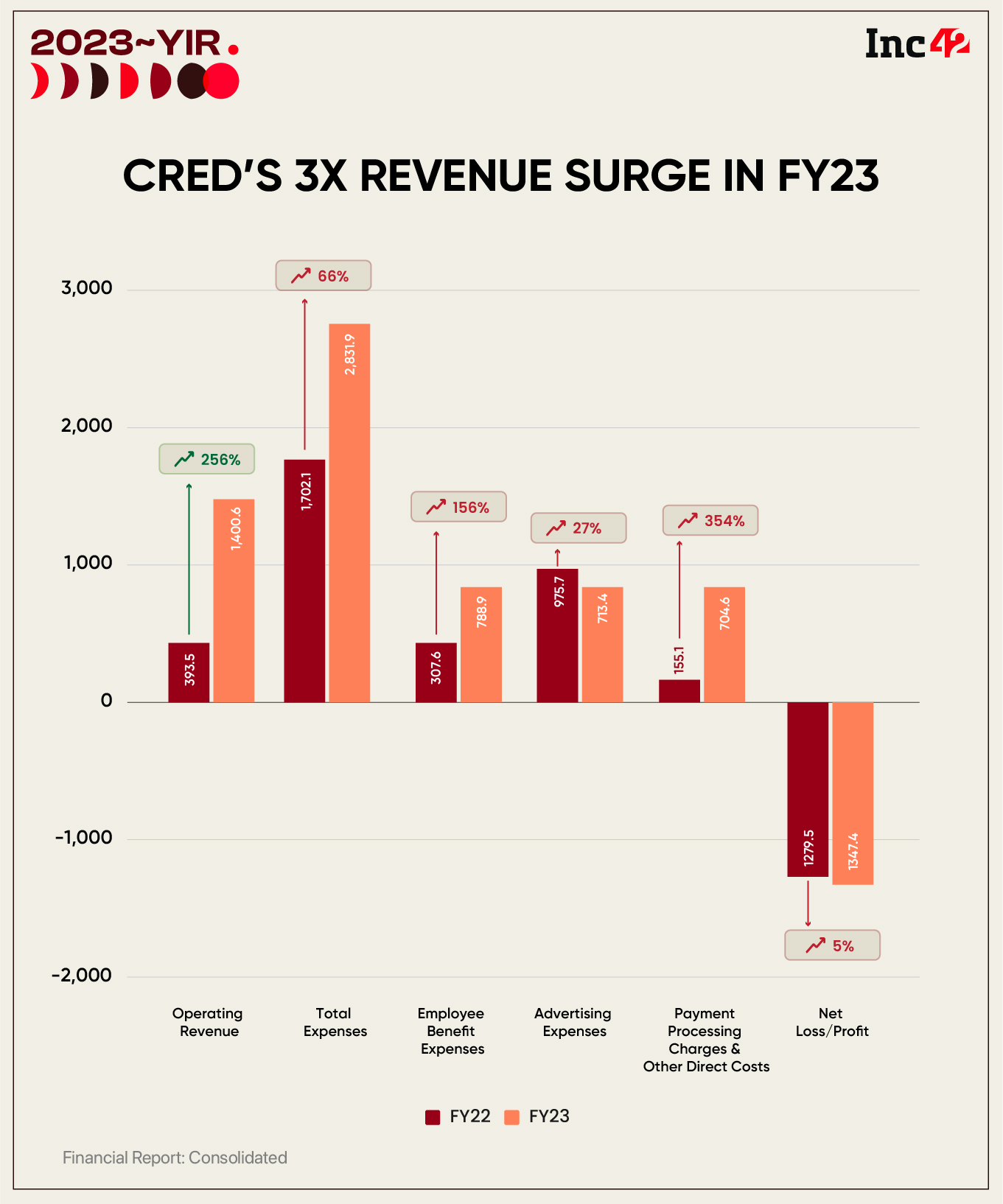

The startup reported a total revenue of INR 1,484 Cr in FY23, a 251.6% increase from INR 422 Cr in the previous fiscal year. On the other hand, losses grew marginally at 5% to INR 1,347 Cr, thanks to expenses growing to INR 2,831.9 Cr from INR 1,702 Cr.

On the engagement side, an average CRED monthly transacting user (MTU) now opens the app more than 20 times a month, which the company claims is one of the best in the industry.

One-third of the credit card bill payments by value were done on CRED, we were told and on a unit economics level, CRED spent INR 2 to earn every single rupee from operations.

That’s a major improvement from INR 4.3 it spent last year to earn a rupee of operating income. So, there have been some measurable improvements for CRED in the past 12-16 months, and new products are very clearly a part of it.

Sampat says CRED’s financial prudence is not new, and in fact the company is CM1 positive for seven quarters now and CM2 positive for five quarters (as of December 2023). These are of course the fundamentals that indicate the right trajectory from a unit economics point of view. And these metrics will be sacrosanct — or in other words, they won’t be sacrificed for growth.

As for EBITDA breakeven, Sampat says it’s a choice. “We ask ourselves whether we want to invest in growth, because there are three new products where we can really make a lot of money. And Amazon is a classic example of that, right?”

He also reveals that CRED is ahead of plan on EBITDA breakeven, without stating any timelines for when that might be announced. Perhaps, it’s the company’s shyness for labels that’s once again surfacing here.

“Until Google went public, people were like what is this stupid company which doesn’t make money, but then we saw the larger vision and the business. Similarly for Amazon or Apple. We are not in a hurry to claim profitability, because our mission is to have the biggest share of the profits in the industry in the long run.”

The analogy we were given is of Apple or Mercedes. The best companies in the world take their time because they are pushing the envelope on products. Whether that be a car or a smartphone or laptop or indeed a fintech app. These titans of industry have earned the right to garner the largest share of profits or goodwill among customers.

Of course, success is a factor of the work and not just patience. The key Sampat believes will be to fight, perform and deliver every day; becoming less and less quiet about the progress. And then perhaps CRED might not shy away from labels as much.

The post Five Years In The Making: CRED’s Year Of Vindication appeared first on Inc42 Media.

No comments